Angel Investing vs. Venture Capital

Why the bar is so different

*Angel investor: a high-net-worth individual who provides financial backing for small startups or entrepreneurs, typically in exchange for ownership equity in the company

*Venture capitalist: a private equity investor that provides capital to companies with high growth potential in exchange for an equity stake

*Source: investopedia

Observe the careers of successful venture capitalists. Most of them began angel investing while operating a company. Some even became well-documented super angels, including the likes of Ron Conway (SV Angel), Peter Thiel (Founders Fund), and Brianne Kimmel (Worklife VC).

Others take the opposite path. I for example, started off in venture capital, and made my way to angel investing. Angels and venture capitalists (VCs) both invest in startups. They both provide advice. They can move from one to the other - VC to angel and vice versa. The definitions after all, look eerily similar. Is there truly a difference?

They are substantially different.

Let’s assume that angel investing would be the best way to become a VC. You get reps meeting founders, deploy capital for an ownership stake, and you support the company along the way. Exactly what a VC does, right?

The act of angel investing does provide all of the above, on the surface. The network and reputation angels develop can open the door to becoming a venture capitalist. However, once in VC, the game is much different.

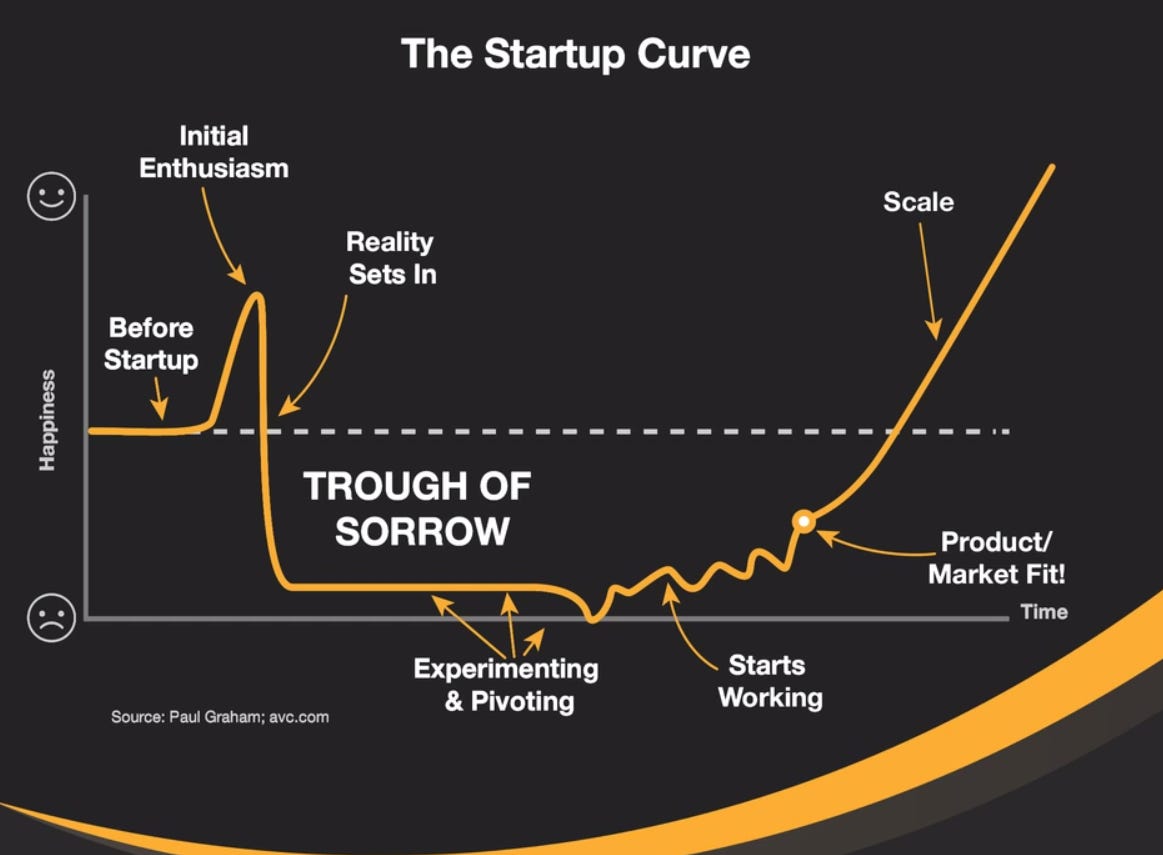

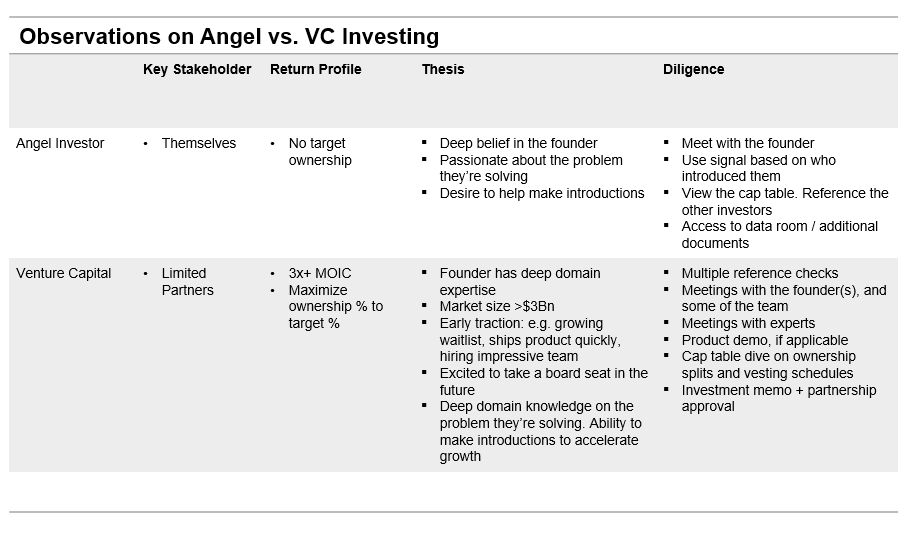

Difference #1) The stakeholders. Purpose is guided by who someone works for. For angels, they are their own boss. Their purpose is to do whatever makes them happy. Is it making the highest return possible? Being involved in solving interesting problems? Helping catalyze someone else’s potential? The angel (and maybe their spouse) decides. Perhaps for this reason - that angels typically invest in areas they are passionate about - a great angel investor provides signal and significantly increases the probability of subsequent fundraises. According to the Kauffman Foundation, a 25% increase to be exact. They are crucial in helping founders through the trough of sorrow, and finding the initial set of customers or believers.

In venture capital, the investor’s purpose is to return capital to their boss: limited partners. This can (and should) be done while making the world a better place, but the return profile is what separates the failed firms from the successful ones.

You don’t see venture capital dollars in small businesses. The market size for a local home goods store is less than the size of the local economy. VCs will know that $100,000 a year in sales might lead to a company valued at $300,000 (assuming 3x revenue). So if you own 10% of that company, you only receive $30,000 upon exit (minus fees), a very very tiny amount for a firm that needs to return millions to billions of dollars to limited partners. Most large-scale VCs look for at least $3Bn in market size before investing.

Meanwhile, if an angel investor invests $10,000 in a company, they are simply looking for some multiple return on that money (if that at all, since most companies fail). The angel is simply comparing returns vs. the average ~8% return of the S&P 500, or any other common investments, a low bar when you think about how quickly tech companies grow.

That’s not to say that angel investing cannot be extremely lucrative. Peter Thiel’s $500K investment in Facebook turned into more than $1 billion in cash. It’s simply to say that angel investors typically have a lower minimum rate of return when investing in a company.

Difference #2) Thesis building. Angels do not see as many companies as one does when working at a venture capital firm. Angel investments often come from a tight network. So angels invest in a) people they believe deeply in, and b) where they personally have some attachment to solving that problem, despite not having the expertise to do so.

At a firm, VCs are maniacally focused on being a good steward of capital. This means investing in people with deep domain expertise or a unique idea. People with a deep story and something to prove. It means making sure the market size is large enough to return the fund if the idea works, and digging into Key Performance Indicators, or anything that can show signs of early traction.

Difference #3) The diligence process. Angel investors are careful to avoid burdening the founder with too much besides access to the data room and documents. Most angels assume the lead investor will do most of the leg work, including issuing the term sheet.

In venture capital, especially for large check sizes, it is crucial to dig into the data and the people. This means multiple meetings, product demos, reference calls, and negotiations on cap table and terms of investment. The process is more arduous but necessary as a fiduciary.

The Benefits

Let’s touch on the benefits of both methods. Angel investors have a better shot at thinking differently. They’re not prone to FOMO or finding the ‘hottest’ deals in the space. Rather, they have a choice. They can do that or follow their own passion and way of thinking; look for the best people to be associated with; have a fun time investing and backing their ideas; and /or only investing in spaces related to the area they work in.

VCs meanwhile, have many more tools at their disposal to run diligence and see a high volume of companies. Large scale firms can leverage their network much further to help founders. And the best firms sit at the nexus of the smartest ideas across verticals. For example, a biotech investor digging into CRISPR technology, likely has a unique advantage of seeing the best applications across the space.

Angel investing is needed and a great tool to learn about investing. However, the bars for angel investing and venture capital investing are at very different heights.

The Diversity Angle: Where are all of the Black Angel Investors?

There are not a lot of people of color that angel invest, especially African Americans. I had not heard of angel investing in tech prior to entering venture capital as a career. The history of angel investing is rooted in tight-knit networks and access to technology companies and VC firms. The landscape is changing with the likes of Blk VC, First Round, Acrew / Concrete Rose and others opening the doors for operators to become angel investors. Focus also surrounds athletes and celebrities, perhaps due to regulatory diversity board requirements, or ideas that have gained traction like the Cultural Leadership Fund out of Andreessen Horowitz.

All of this represents great progress. However, the main structural barrier comes in the form of regulatory protections. The SEC requires that angel investors be accredited. This usually means greater than $1M in net worth, making over an annual income of at least $200,000, or $300,000 if combined with a spouse’s income, or being a “knowledgeable employee” with a Series license. It is meant to be a proxy for know-how to handle the risks involved. Yet, given the generational wealth divide that exists, the number of African Americans that reach the status of accredited investor is few and far between. Akin to the democratization of access to the stock market we have seen over the last 20 years, the market should embrace another way to vet a retail investor’s understanding of the risks associated with angel investing, while allowing them to have access to this market, lest we find ourselves driving the generational wealth divide even further.

Disclaimer: The above is an opinion and for information purposes only. It is not intended to be investment advice. Seek a duly licensed professional for investment advice.

Great article. Have you heard of Cap Table Coalition? Would encourage you to check them out! https://www.captablecoalition.com/